Finance and risk¶

Robust covariance is especially useful in finance because returns are heavy-tailed, correlated, and sensitive to stress regimes.

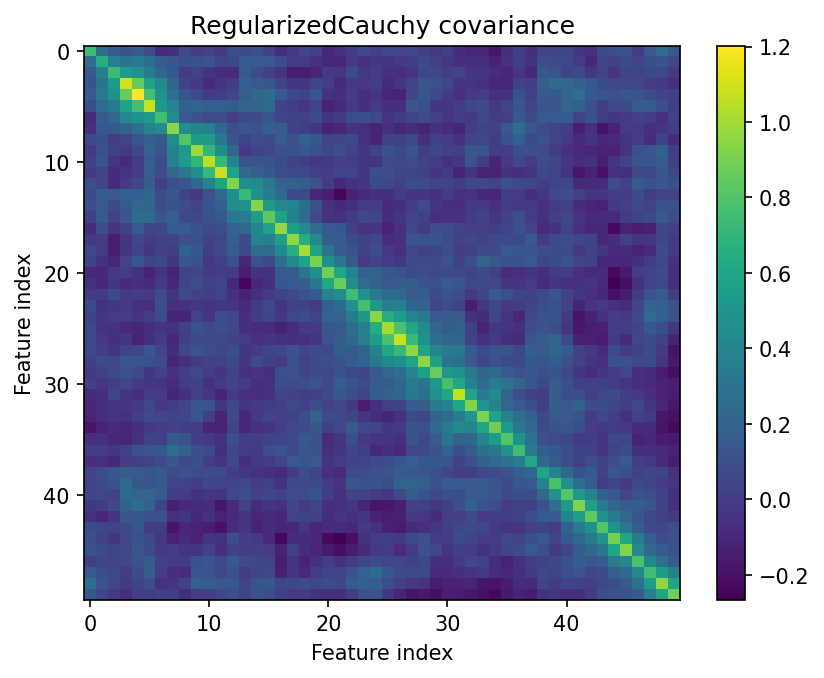

Finance risk covariance

Small-sample heavy-tail covariance for multi-asset return features.

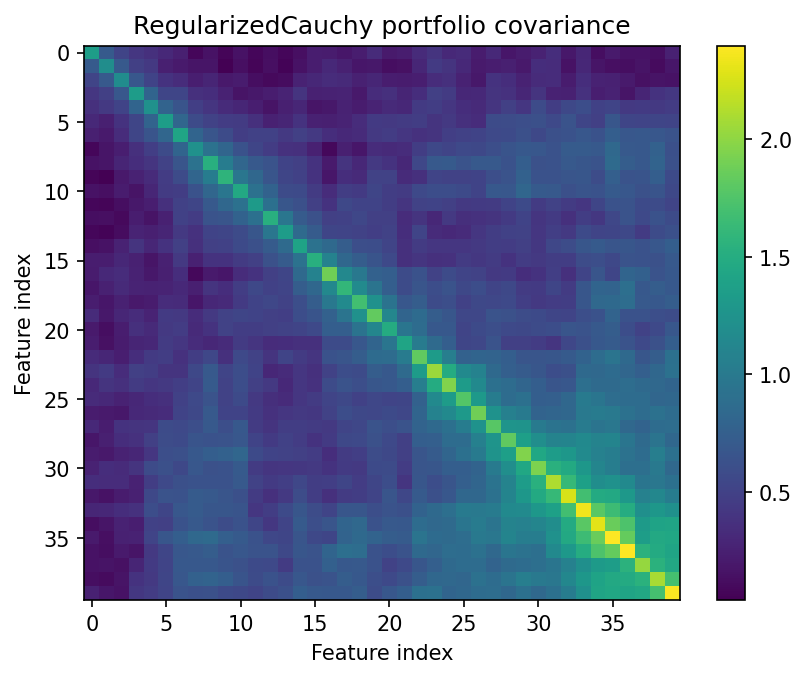

Portfolio stress monitoring

Compare empirical and robust risk estimates under stress contamination.

How to use this topic¶

Start with the first card if you want the simplest demonstration. Then move to the more specialized page when the data shape matches your problem. Every page includes captured output, plots, interpretation notes, and a command to reproduce the result.