Rolling-window finance anomaly detection¶

Why this result matters¶

Single-day outliers are useful, but many financial anomalies are regimes: periods of unusual volatility, correlation, drawdown, or cross-asset behavior. This example converts price data into rolling-window features and scores each window with robust distances.

What the data represent¶

This documented run uses the same reproducible synthetic price table as the single-day market-stress example. The script forms 20-trading-day windows with a 5-day step, producing 176 windows over 8 assets.

Command¶

python examples_external/finance_rolling_window_anomaly.py \

--prices examples_external/data/prices.csv \

--window 20 \

--step 5 \

--outdir results/external/finance_rolling_window

Output from the run¶

rolling-window finance anomaly detection

method,n_windows,window,step,n_assets,detected_windows,threshold,max_distance,radial_kurtosis

RegularizedCauchy,176,20,5,8,5,152.36606980024123,214.0264973740177,3.9770869272091005

top anomalous windows

rank,start_date,end_date,robust_distance

1,2020-09-03,2020-09-30,214.0264973740177

2,2020-08-27,2020-09-23,195.33176540660608

3,2020-09-10,2020-10-07,186.5938392771558

4,2022-09-01,2022-09-28,171.02390217029944

5,2022-08-25,2022-09-21,158.04725685375985

6,2020-08-20,2020-09-16,142.89742471104356

7,2021-08-05,2021-09-01,139.78449227022205

8,2021-08-12,2021-09-08,139.28137467369586

9,2020-12-03,2020-12-30,138.04402746304234

10,2022-09-08,2022-10-05,136.06979631136875

saved outputs to results/external/finance_rolling_window

Summary metrics¶

Method |

Windows |

Window length |

Step |

Assets |

Detected windows |

Threshold |

Max distance |

Radial kurtosis |

|---|---|---|---|---|---|---|---|---|

RegularizedCauchy |

176 |

20 |

5 |

8 |

5 |

152.37 |

214.03 |

3.98 |

Plots¶

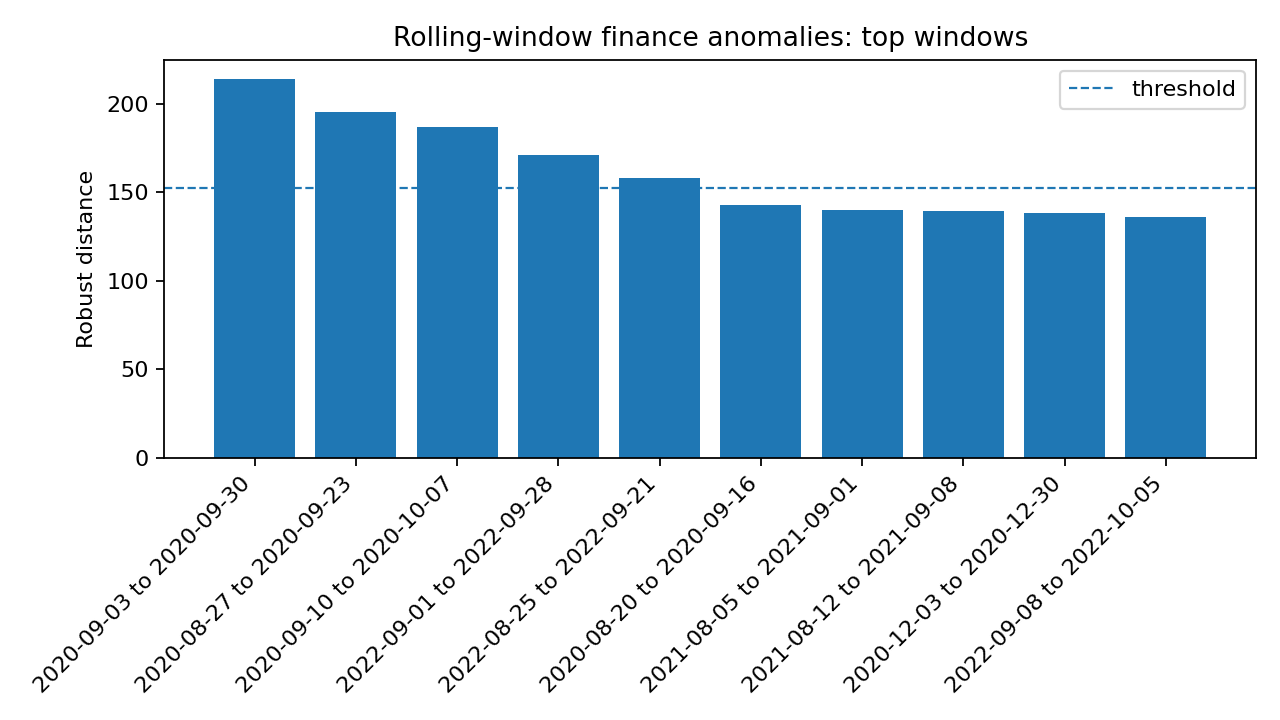

Top anomalous rolling windows. The top three windows overlap the September 2020 stress period, showing that the method detects regimes rather than only isolated points.¶

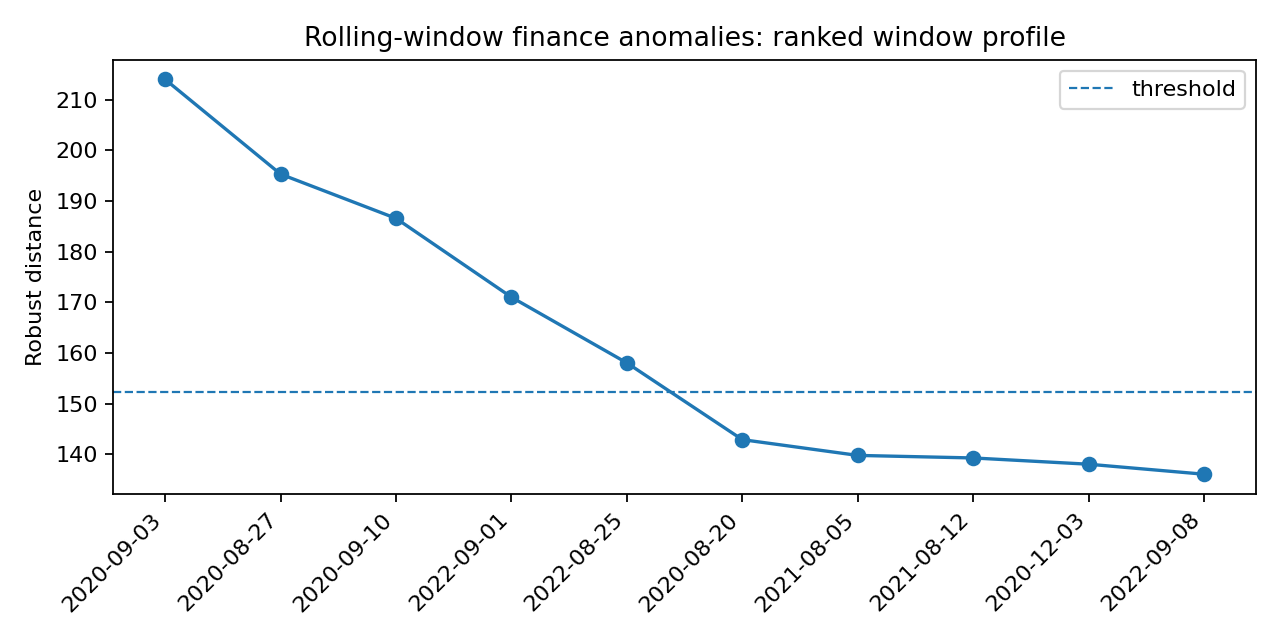

Ranked window-level robust-distance profile. Windows above the threshold are the first regime candidates to inspect.¶

Interpretation¶

The rolling example detects 5 windows above the threshold. The top windows are:

Rank |

Start date |

End date |

Robust distance |

|---|---|---|---|

1 |

2020-09-03 |

2020-09-30 |

214.03 |

2 |

2020-08-27 |

2020-09-23 |

195.33 |

3 |

2020-09-10 |

2020-10-07 |

186.59 |

4 |

2022-09-01 |

2022-09-28 |

171.02 |

5 |

2022-08-25 |

2022-09-21 |

158.05 |

The top windows overlap strongly, which is a useful signal in time series: a single anomalous day can be noisy, but repeated high-scoring overlapping windows suggest a persistent regime change.

Why this estimator¶

Use RegularizedCauchy when windows are high-dimensional or heavy-tailed. If

window features are smoother and closer to elliptical Student-t behavior, try

StudentTScatter as a sensitivity check.

Production notes¶

For real markets, use rolling-window anomalies as a monitoring layer. Review clusters of high-scoring windows, not just one row at a time. Consider adding volatility, drawdown, correlation, and sector-return features before fitting the robust scatter model.