Finance market-stress anomaly detection¶

Why this result matters¶

Financial returns are heavy-tailed and correlated across assets. A single large move in one asset is not always a market anomaly, but an unusual cross-asset return vector can indicate stress, regime change, a macro shock, or data-quality problems. Robust covariance gives an interpretable score for each trading day: the robust Mahalanobis distance from the central market regime.

What the data represent¶

This documented run uses a reproducible synthetic price table with 899 return days and 8 assets. The generator injects stress-like periods so that the script can be run without downloading Yahoo/Kaggle data while still producing a finance-shaped example.

The input format is a CSV with one date column and one numeric price column per asset:

date,SPY,QQQ,IWM,TLT,GLD,EFA,EEM,HYG

2020-01-01,100.0,...

Command¶

python examples_external/finance_market_stress.py \

--prices examples_external/data/prices.csv \

--outdir results/external/finance_market_stress

Output from the run¶

finance market-stress anomaly detection

method,n_days,n_assets,alpha,detected_days,threshold,max_distance,median_distance,radial_kurtosis,condition_number

RegularizedCauchy,899,8,0.975,23,95.79757169861077,251.5634271621798,7.344121400847285,2.815129834185989,6.066016648802037

top stress days

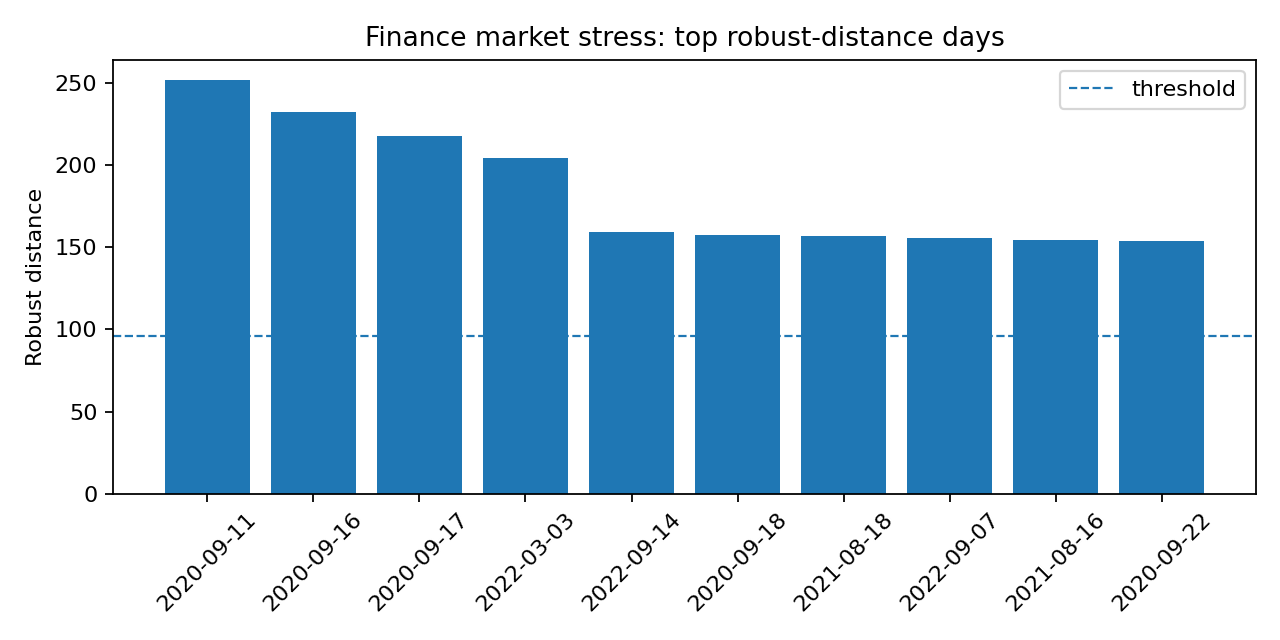

rank,date,robust_distance

1,2020-09-11,251.5634271621798

2,2020-09-16,232.6356115298036

3,2020-09-17,217.49733699014894

4,2022-03-03,204.18076327111973

5,2022-09-14,159.49903060794182

6,2020-09-18,157.19605603272385

7,2021-08-18,156.86350751922998

8,2022-09-07,155.85245060739706

9,2021-08-16,154.16973914961375

10,2020-09-22,154.1142504102232

saved outputs to results/external/finance_market_stress

Summary metrics¶

Method |

Days |

Assets |

Alpha |

Detected days |

Threshold |

Max distance |

Median distance |

Radial kurtosis |

Condition number |

|---|---|---|---|---|---|---|---|---|---|

RegularizedCauchy |

899 |

8 |

0.975 |

23 |

95.80 |

251.56 |

7.34 |

2.82 |

6.07 |

Plots¶

Top ranked robust-distance days. The dashed line is the detection threshold. The largest detected day is 2020-09-11 with robust distance 251.56.¶

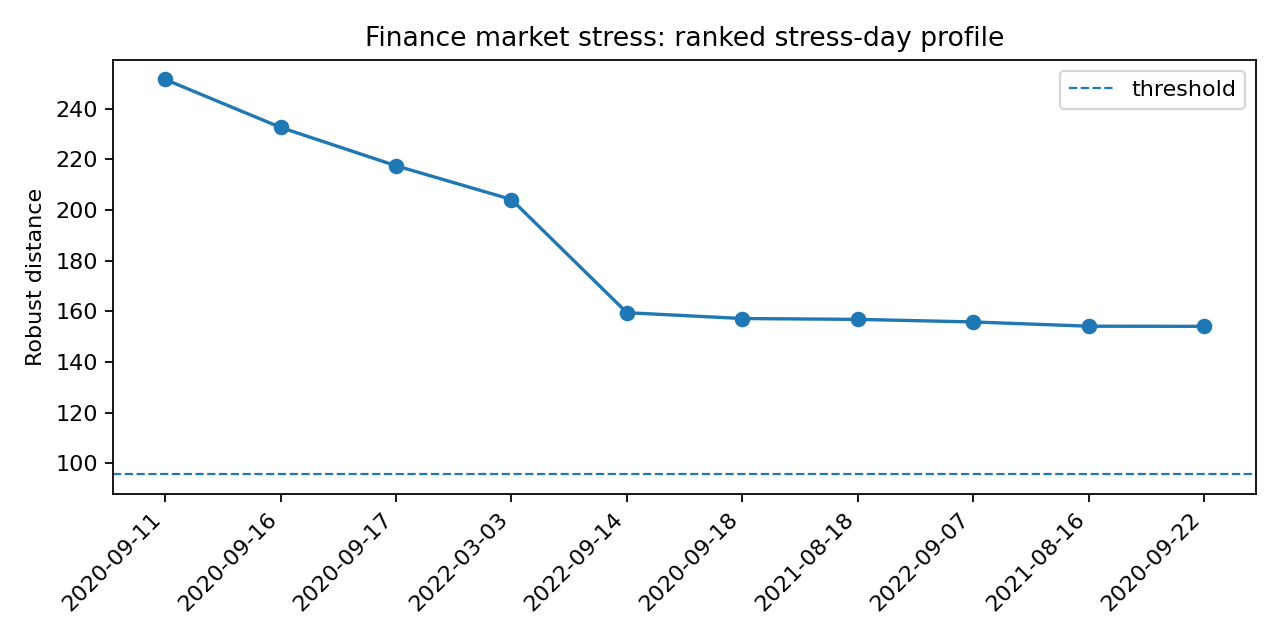

Ranked stress-day profile for the top detected dates. A finance user can inspect the dates directly and compare them against known market events or injected stress periods.¶

Interpretation¶

The estimator flags 23 of 899 days, about 2.6%, which is consistent with the

alpha=0.975 threshold. The condition number is low (about 6.1), so the

robust covariance estimate is numerically stable. The radial kurtosis is not

extreme, meaning the robust fit has absorbed the central heavy-tailed behavior

without becoming ill-conditioned.

The top stress days cluster around stress-like periods, especially September

2020 and September 2022 in this synthetic run. This makes the result easy to

explain: robustcov is not only returning a score, it is producing a ranked

list of market days for review.

Why this estimator¶

Start with RegularizedCauchy for finance returns because it combines strong

radial downweighting with shrinkage. Use StudentTScatter as a smoother

heavy-tail sensitivity check, and AutoRobustScatter if the data regime is

unclear.

Production notes¶

For real data, run the same script on ETF or stock prices. Review top days against market calendars, corporate actions, missing prices, and known stress events. For portfolio use, robust distances should complement risk models; they should not be treated as trading signals without validation.