External and Kaggle gallery¶

This page is the single entry point for optional Kaggle and external-data examples. These examples are not part of tests because they require manual downloads, dataset-specific licenses, or larger local files.

The goal is not to claim that robustcov wins everywhere. The goal is to

show where robust covariance gives a strong advantage, where it is competitive,

where it is mainly diagnostic, and where another method is better.

How to read the cards¶

Label |

Meaning |

|---|---|

Strong win |

robustcov clearly improves the most relevant metric against common unsupervised baselines. |

Competitive |

robustcov is close to the best method, or wins one metric but loses another. |

Competitive, slow |

robustcov improves quality but runtime is currently a weakness. |

Not best |

another baseline performs better; the robustcov result is still reported for transparency. |

Diagnostic |

there are no ground-truth labels, but robust distances provide interpretable stress/anomaly rankings. |

Recommended result pages¶

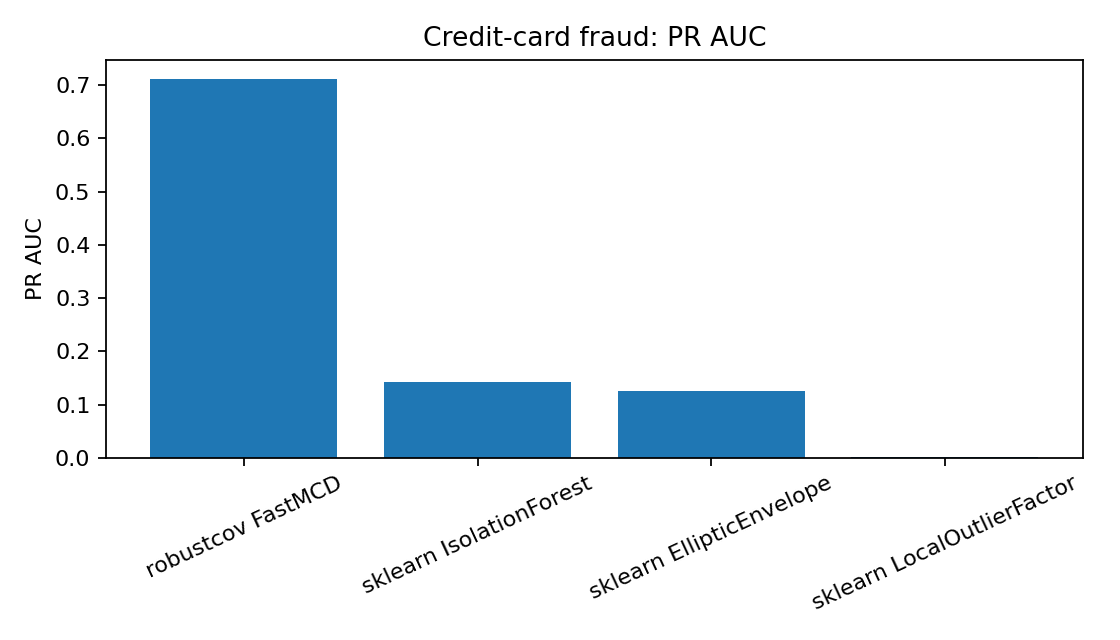

Credit-card fraud

Strong win. FastMCD PR-AUC 0.712 and F1 0.801 on a classic imbalanced fraud dataset.

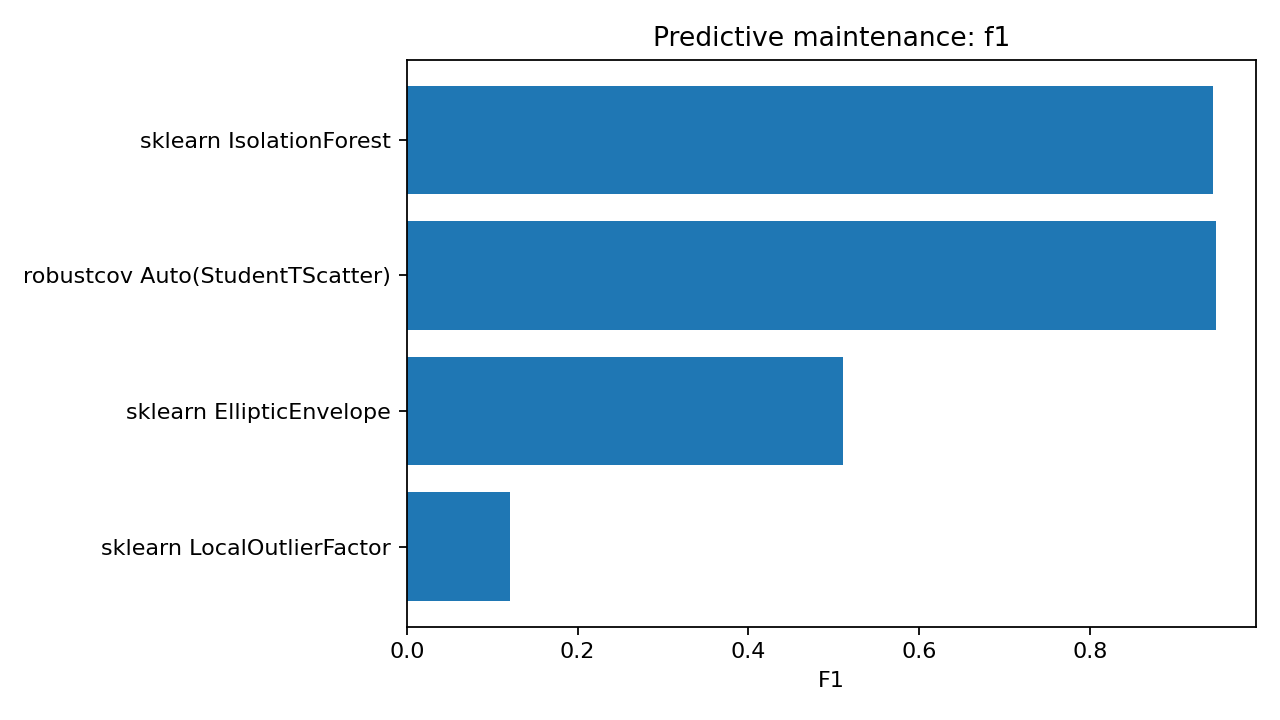

Predictive maintenance

Competitive. robustcov gives the best F1, while IsolationForest has stronger PR-AUC and speed.

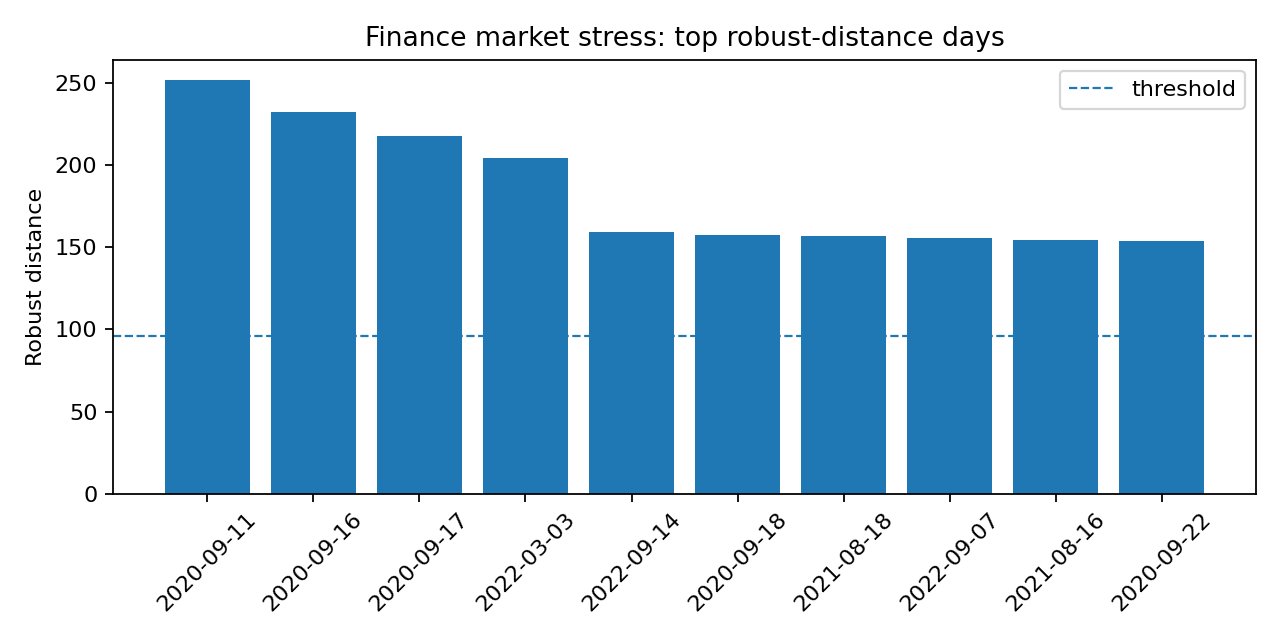

Finance market stress

Diagnostic. RegularizedCauchy ranks unusual cross-asset return days.

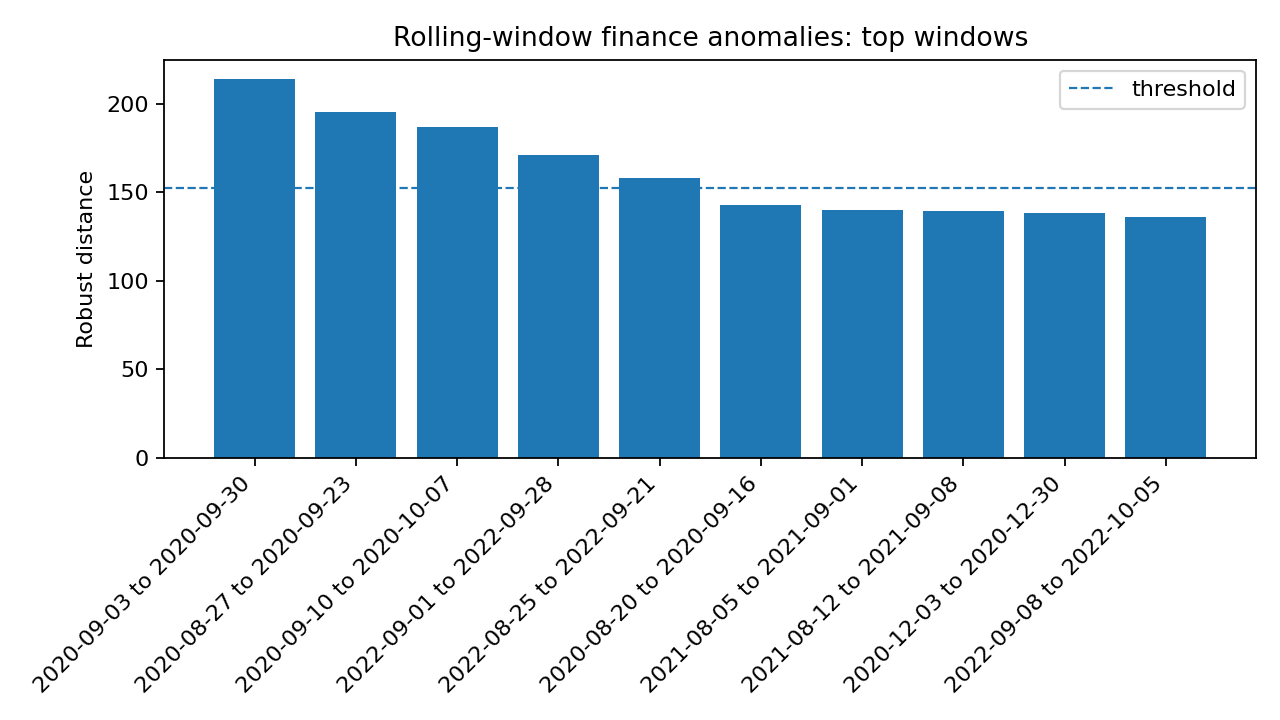

Rolling market regimes

Diagnostic. Window-level features identify abnormal volatility/correlation regimes.

Honest secondary results¶

Current documented external results¶

Dataset / example |

Status |

Main method |

Headline result |

Notes |

|---|---|---|---|---|

Credit-card fraud |

Strong win |

FastMCD |

PR-AUC 0.712, F1 0.801 |

Large metric gap vs common sklearn anomaly baselines. |

Predictive maintenance |

Competitive |

Auto(StudentTScatter) |

F1 0.947 vs IsolationForest 0.944 |

IsolationForest is faster and has better PR-AUC. |

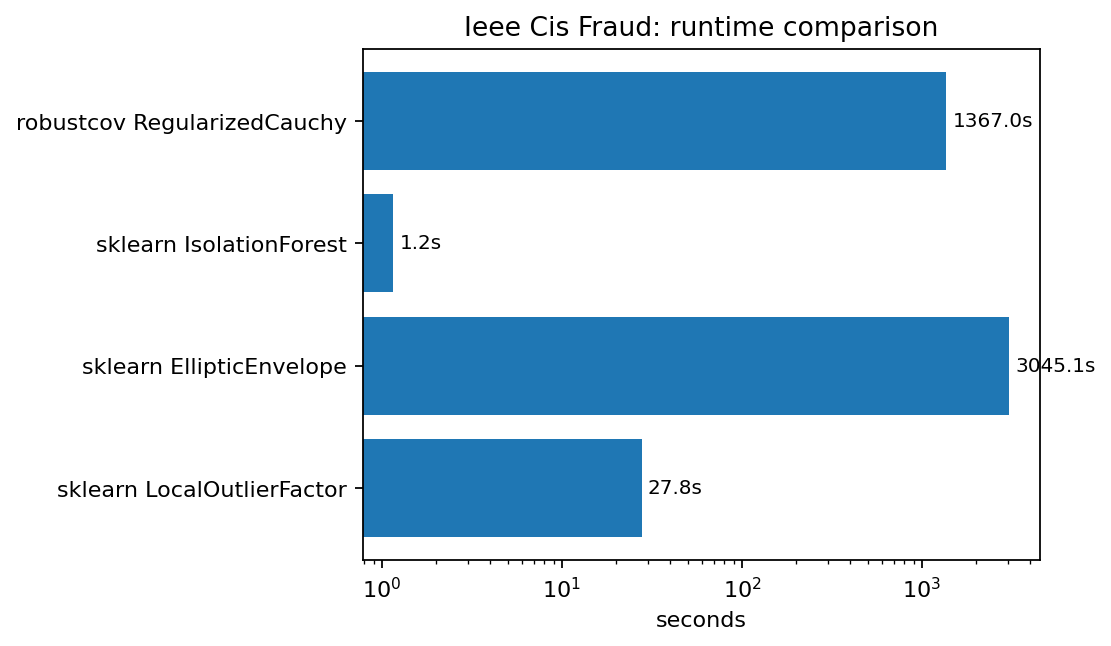

IEEE-CIS fraud |

Competitive, slow |

RegularizedCauchy |

PR-AUC 0.093 vs IsolationForest 0.084 |

Best tested unsupervised quality, but much slower. |

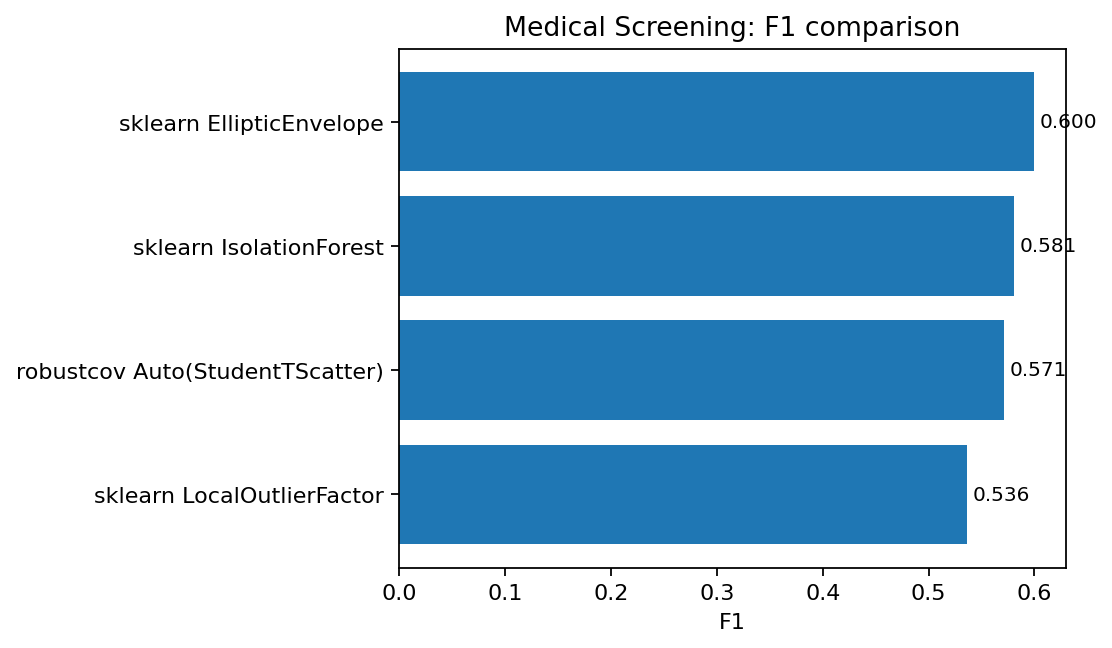

Medical screening |

Not best |

Auto(StudentTScatter) |

PR-AUC 0.567 vs EllipticEnvelope 0.629 |

Honest negative/diagnostic result. |

Finance market stress |

Diagnostic |

RegularizedCauchy |

23 / 899 days detected |

Top days cluster around stress-like periods. |

Rolling-window finance |

Diagnostic |

RegularizedCauchy |

5 / 176 windows detected |

Top windows cluster around September stress regimes. |

Why UNSW-NB15 is not highlighted¶

The commonly used UNSW-NB15 training split can contain a very high attack

fraction. That makes it less like rare-anomaly detection and more like

unsupervised or semi-supervised classification. robustcov may still be

useful there as a risk-ranking diagnostic, but it is not a clean headline

anomaly benchmark for this package. We therefore do not highlight it in the

external gallery.

Run external examples¶

External examples are optional and dataset-dependent. The recommended path is:

python examples_external/<script>.py --data path/to/data.csv --outdir results/external/<name>

python examples_external/collect_external_results.py \

--root results/external \

--outdir results/external_registry

The scripts, dataset notes, and notebook templates live under examples_external/.

They are intentionally outside the core test suite because Kaggle datasets have

separate licenses, download steps, and file sizes.